TL;DR

- Enterprise procurement AI was framed as depth vs speed — it was a false choice. The trade-off CPOs thought they had to make never actually existed.

- AI-native platforms nailed intake, missed fulfillment. Great front door, not enough depth behind it.

- Enterprise suites had depth, but bolted AI on top. Real substrate, non-native agentic layer.

- Accumulated depth became the unfair advantage. Agentic AI needs governed data, deterministic workflows, and contextual specificity — things deep S2P suites already had.

- The winning architecture is three layers. Guided Intake + native Agentic Platform + deep S2P suite — the shape of Zycus’s Merlin Agentic Platform.

- Gartner, Forrester, IDC, and Hackett agree. Four independent lenses, one Leader.

The race is already over. Decided by architecture years ago, not by 2026 demos.

The trade-off everyone assumed was permanent turned out to be a category mistake. Here’s what the depth-or-speed argument missed — and why the platforms that figured it out have already crossed the finish line.

For the, every CPO sitting through an agentic procurement RFP has faced a shortlist organised into two camps that seemed to demand opposite trade-offs.

In one camp: AI-native platforms, often built in the last three to four years, designed from the ground up around conversational interfaces and agentic execution. Beautiful intake. Natural-language requests. Fast deployment. Demos that captured the imagination of business users who were tired of portals nobody wanted to use.

In the other camp: enterprise S2P suites, accumulated over a generation of category-by-category refinement. Deep workflow rigour. Global compliance coverage. Mature integrations across the universe of ERPs and tax engines. Decades of edge-case handling that no startup had yet encountered.

Both camps were making valid arguments. The conventional wisdom said the trade-off was structural — depth or speed, pick one. The two requirements seemed to demand opposite kinds of organizations: the patient enterprise builder and the fast-moving AI-native startup. No single vendor could be both.

What the conventional wisdom missed is what this piece is about.

Read more: Strategies for Large and Medium Enterprises: Mastering Source-to-Pay Before It’s Too Late

What Each Camp Got Right, and Where Each One Stopped

The AI-native camp was right about something the enterprise camp had been slow to admit. For too long, procurement software had been built for procurement teams rather than for the business users who actually needed to buy things. Forms that nobody filled out correctly. Portals that requestors avoided by emailing procurement directly. Approval flows that felt like punishment for trying to follow the process. The AI-native platforms identified the real user — the marketing manager who needs display stands, the engineer who needs lab supplies — and built for that user first. That was a genuine architectural insight, not a marketing one.

Where this camp hit a ceiling was in the depth required to fulfil what intake had captured. A natural-language request for display stands is the easy part. Routing it through a global supplier ecosystem that respects forty jurisdictions of tax law, dozens of contract templates, supplier risk frameworks that pass a regulator’s audit, and category-specific workflows refined across hundreds of customer deployments — that is the hard part. The hard part takes years to build, and most AI-native platforms did not have those years.

The enterprise camp was right about something the AI-native camp couldn’t easily replicate. The accumulated depth of an S2P suite — the workflow primitives, the contract logic, the supplier networks, the compliance engines, the data models that hold up across forty jurisdictions — is not a marketing claim. It is a multi-decade asset. It is the substrate that lets a procurement function actually operate at Fortune 500 scale.

Read more: Flying the Plane While Fixing the Wings: The Procurement Paradox in Emerging Enterprises

Where this camp hit its own ceiling was in how AI was added to the architecture. For most enterprise S2P suites, AI arrived as a layer on top of platforms designed in a pre-agent world. Conversational front doors bolted to monolithic backends. The depth was real. The AI was an attachment.

Two camps. Two valid arguments. Two ceilings.

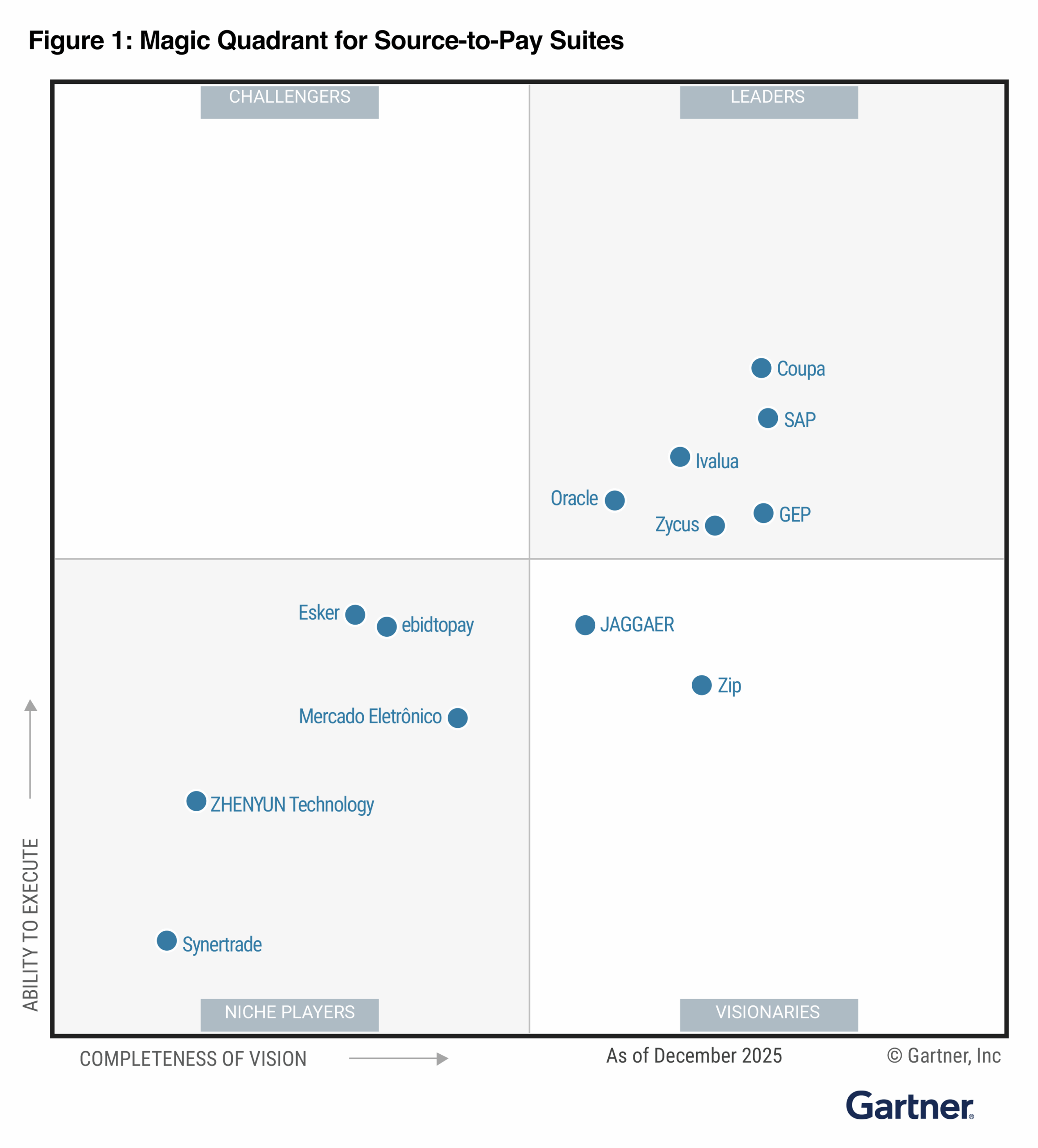

Figure 1 · The procurement AI shortlist as the market saw it — and the category most buyers didn’t expect to find.

The Architectural Physics

The reason the depth-or-speed trade-off has been treated as unavoidable is that it almost is.

Building a procurement platform with the depth a global enterprise demands takes years of category-by-category refinement. You learn how aerospace MRO is different from pharmaceutical raw materials, how compliance varies between jurisdictions, how supplier ecosystems shift over time. None of that can be speedrun. It has to be lived through with customers until the platform’s logic carries the weight of the workflows underneath.

Building an AI-native agentic platform requires a foundation designed for agents from the start — APIs deep enough to expose every workflow primitive, an integration backbone that lets agents communicate across systems, an orchestration layer that coordinates multiple agents in parallel, a unified data core so agents reason on the same facts the rest of the platform operates on. None of that retrofits cleanly onto architectures designed in a pre-agent era. You can wrap a chat interface around almost anything. You can’t wrap an agentic execution layer around a monolith and expect it to behave.

McKinsey’s Global Tech Agenda 2026 surveyed more than 600 technology and business leaders and found a broad shift from episodic efficiency gains to organisational velocity — companies making teams more productive, streamlining workflows, and restructuring technology and operating models. Speed of execution has become the new moat. But what the same survey didn’t say out loud is what every CIO had already figured out — that speed without depth is its own dead end. Pilots that demo well and never scale. Agents that work in isolation and break inside complex workflows.

This is what made the depth-or-speed trade-off feel architectural rather than optional. It wasn’t lazy thinking. It was an honest read of what the two requirements seemed to demand.

So the question that hung over the market through 2024 and 2025 was: if the trade-off was as real as it looked, how did anyone escape it?

The Unfair Advantage Hiding in Plain Sight

The answer inverts a piece of conventional wisdom that had been taken as obvious.

In most software categories, decades of accumulated depth is a disadvantage in the AI era. Older codebases. Monolithic architectures. Teams structured for sustaining maintenance rather than aggressive innovation. The dominant narrative has been that AI-native challengers should win because they are unburdened by legacy weight. In most categories, that narrative is correct.

In procurement specifically, it isn’t.

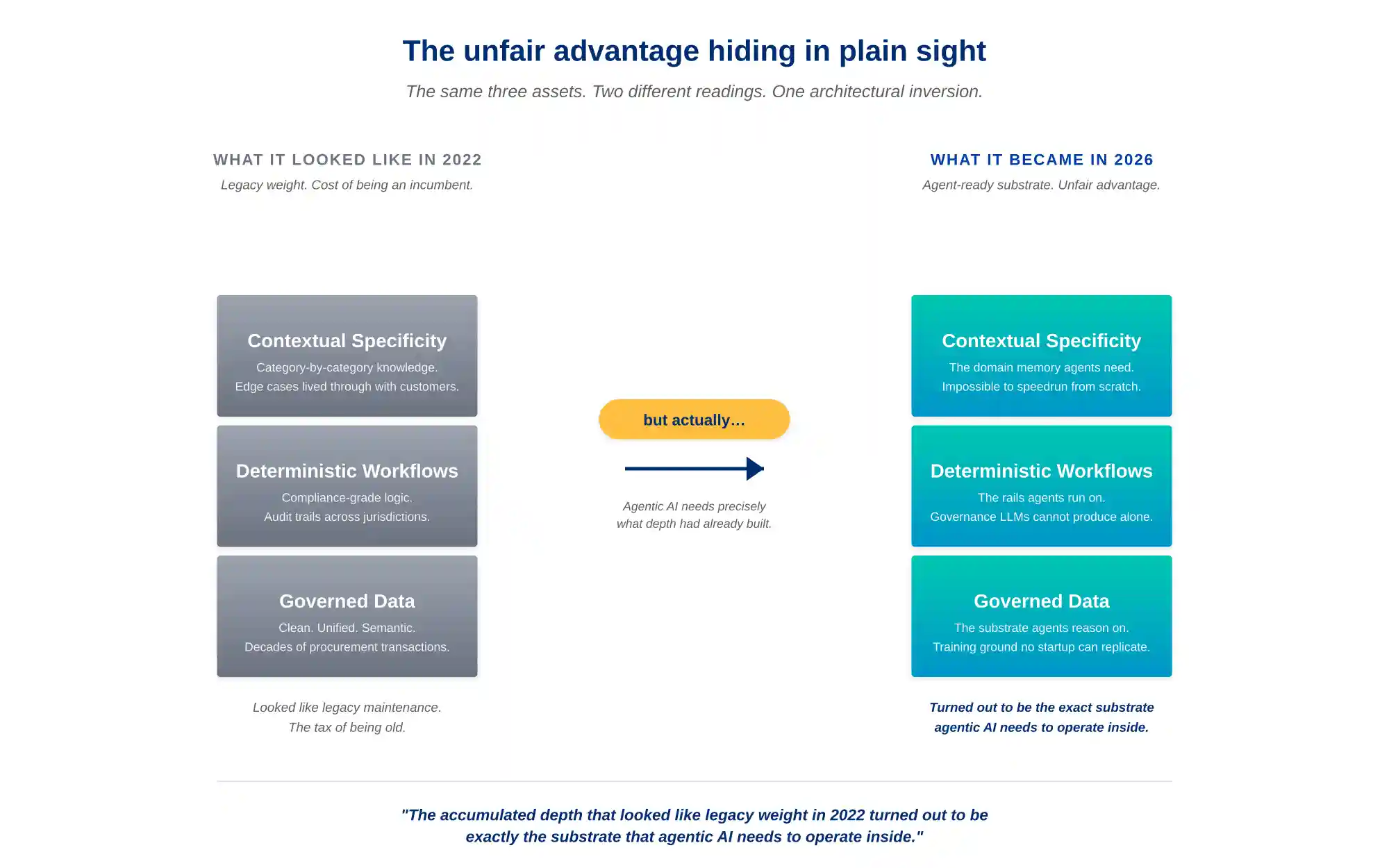

Agentic AI in procurement requires three things that are unusually hard to build from scratch. It requires governed data — clean, unified, structured around the actual semantic shape of procurement transactions, not generic enterprise records. It requires deterministic workflows — the kind that hold up across compliance regimes and audit trails, not the probabilistic-best-effort logic that LLMs produce by default. And it requires contextual specificity — the accumulated knowledge of how a contract clause behaves differently in pharma than in aerospace, how a supplier risk score varies across jurisdictions, how an invoice exception in one country is a routine match in another.

These three things — governed data, deterministic workflows, contextual specificity — are precisely what a deep S2P suite has been quietly accumulating for years. Not because anyone planned for the agentic era. Because procurement is the kind of domain where you cannot ship a product without those things.

The accumulated depth that looked like legacy weight in 2022 turned out to be exactly the substrate that agentic AI needs to operate inside.

Figure 2 · The same three assets, two different readings. The architectural inversion that escaped the trade-off.

This is the inversion the market is still adjusting to. The platforms that combined enterprise depth with startup speed didn’t escape the trade-off through clever engineering. They discovered that the depth was the unfair advantage all along — and the only architectural work left was to build a native agentic layer that could sit on top of it.

What that Combination Actually Looks Like

The architectural shape of enterprise depth and startup speed is specific and traceable.

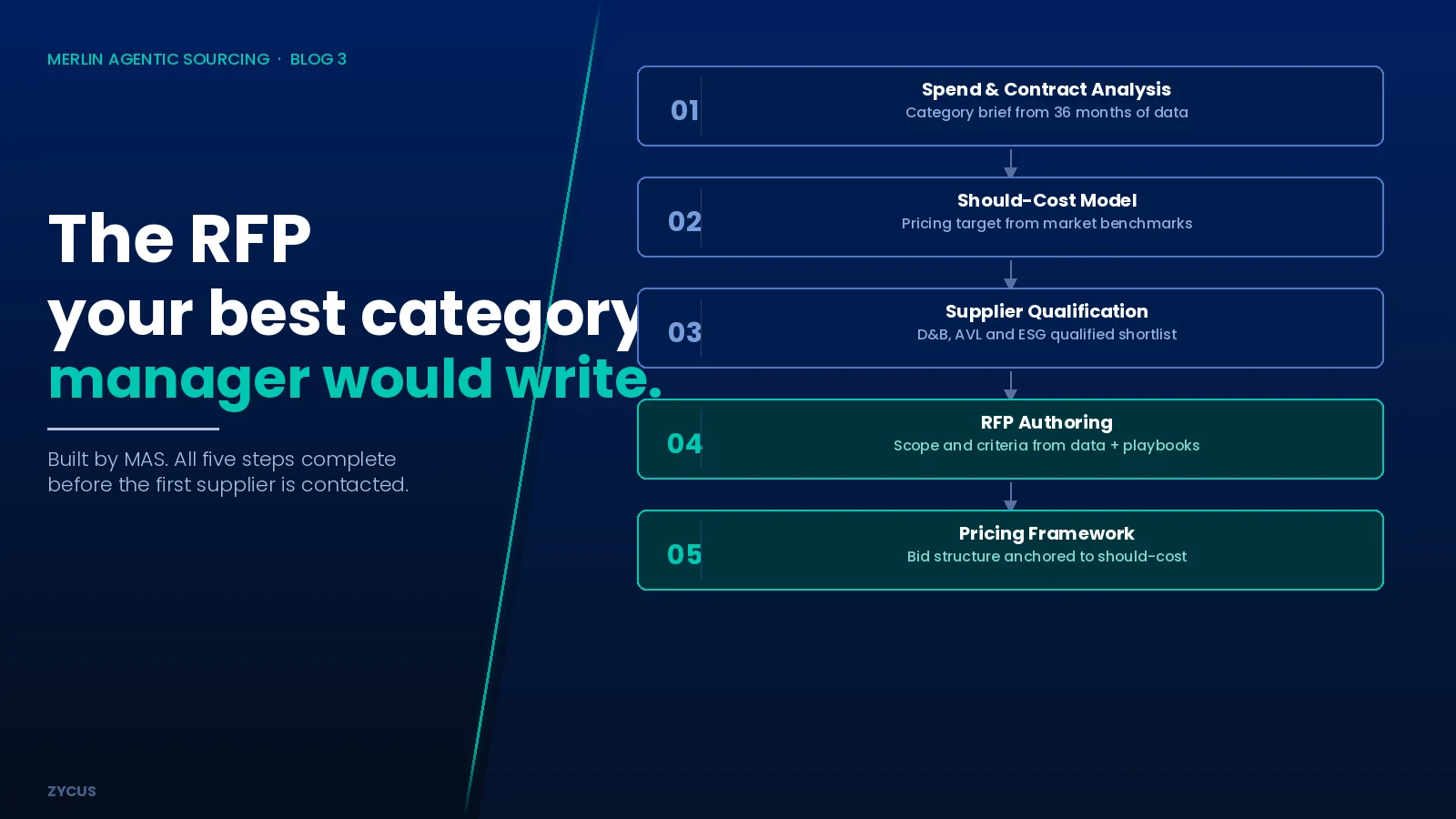

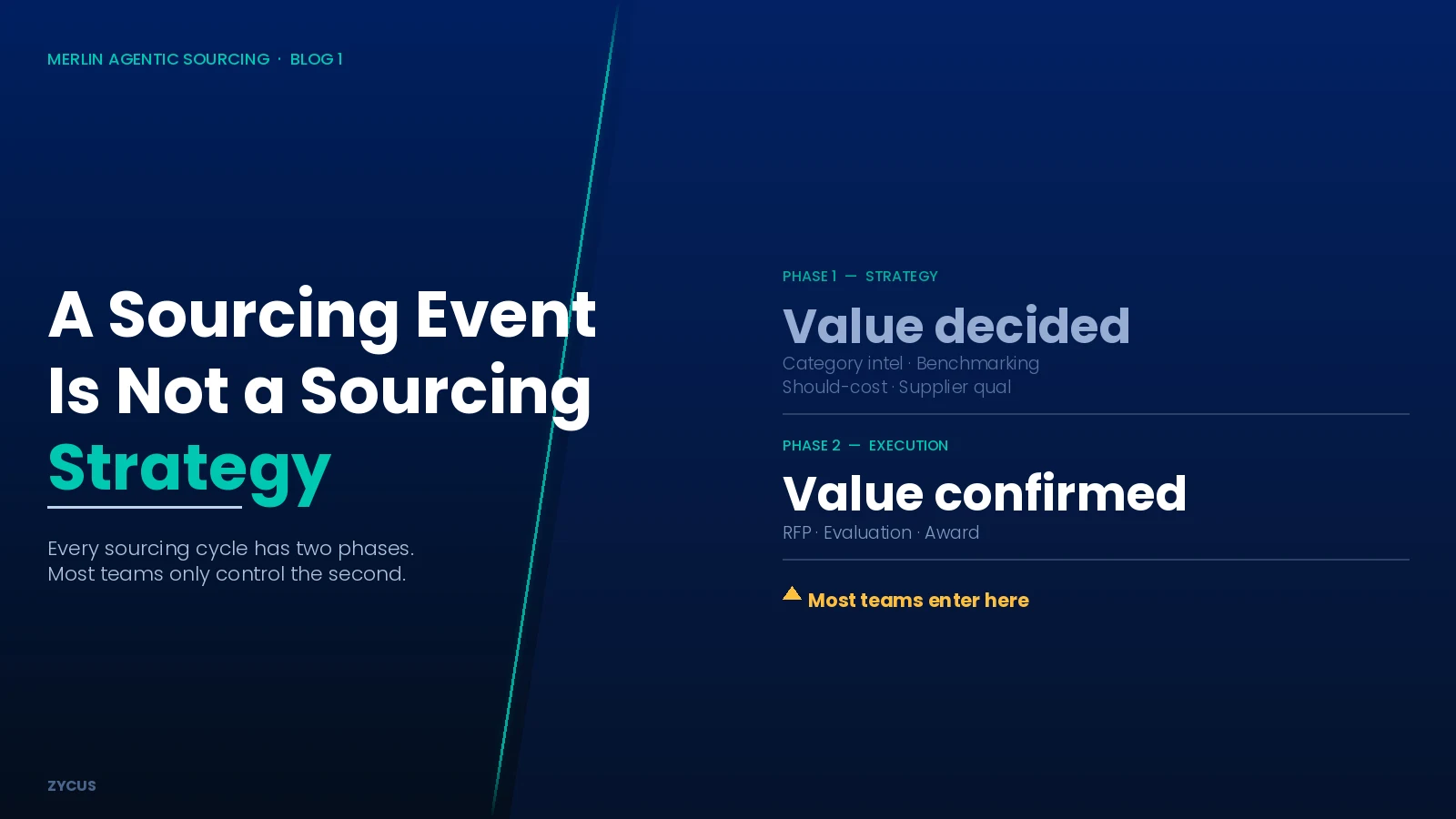

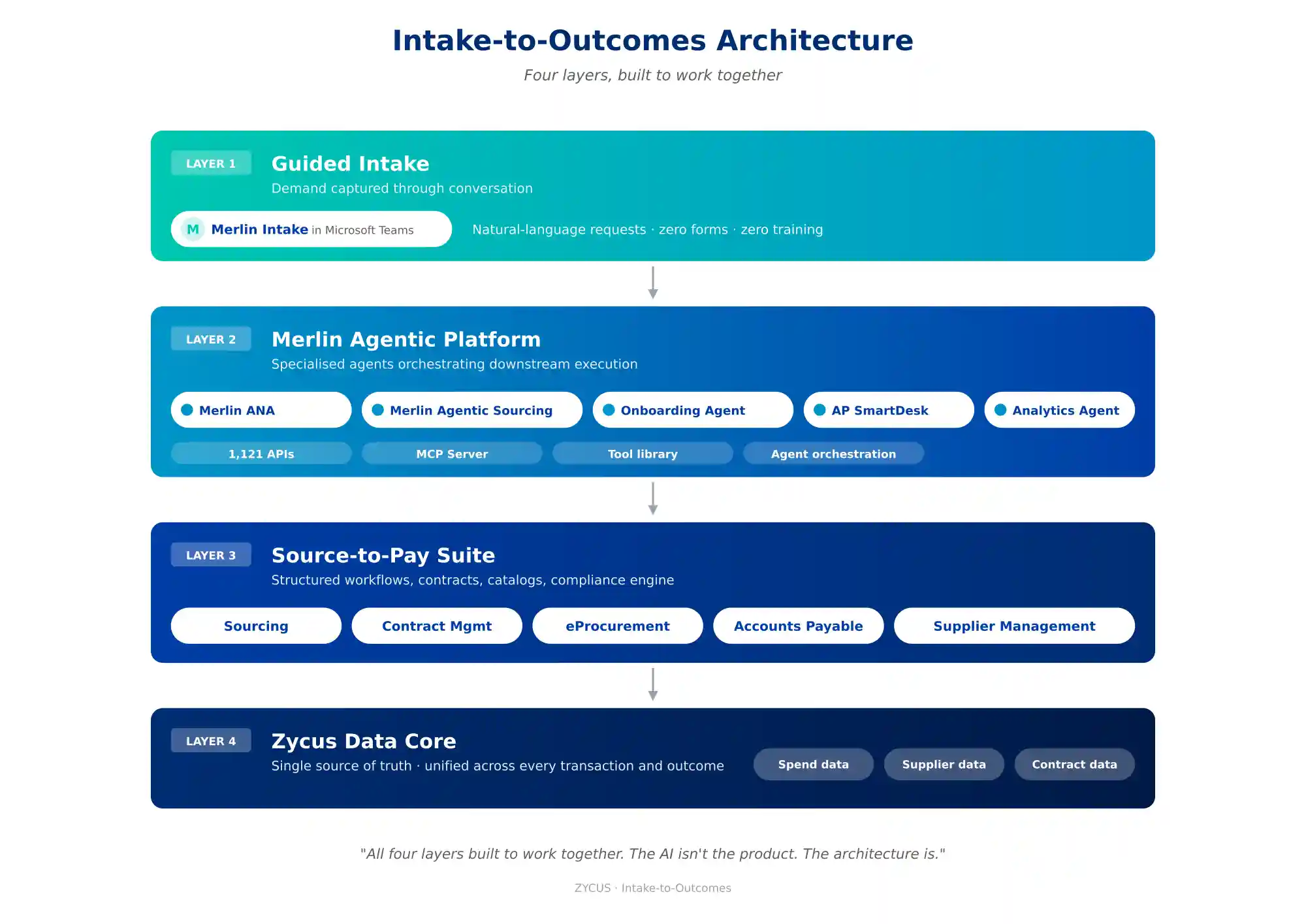

It is a three-layer stack. At the top, a guided intake layer — the conversational front door where any procurement request is captured in natural language, without forms and without training. In the middle, a native agentic platform — specialised agents for autonomous negotiation, agentic sourcing, supplier onboarding, and accounts payable, coordinated by an agent orchestration layer and connected through more than a thousand APIs, a Model Context Protocol server, and a tool library. At the foundation, a deep source-to-pay suite — built up over a generation of category-by-category refinement, compliance-grade workflows, and a unified data core that every agent reasons on.

Zycus’s Merlin Agentic Platform is the architectural exemplar of this pattern. The agentic layer was built natively for multi-agent execution — specialised agents orchestrated across the S2P backbone, not a chat UI bolted onto a pre-agent backend. It connects to the suite through 1,121 APIs, reasons on the unified Zycus Data Core, and operates across the full procurement lifecycle through the Merlin agent family: Merlin Intake, ANA (Autonomous Negotiation Agent), Merlin Agentic Sourcing, AP SmartDesk, and the Autonomous Supplier Onboarding Agent. The three-layer Intake-to-Outcomes architecture — Guided Intake, Agentic AI, and a deep S2P foundation — is the structural expression of depth-plus-speed in a single platform.

Figure 3 · The three-layer Intake-to-Outcomes architecture. Guided Intake at the top, a native Merlin Agentic Platform in the middle, and a deep S2P suite — with the Zycus Data Core as unified data spine — at the foundation.

The clearest evidence that something architectural happened is that the market’s independent referees noticed it independently. Over the last eighteen months, three major analyst firms — Gartner, Forrester, and IDC — have each placed Zycus in their leader positions, and The Hackett Group has partnered with Zycus on the definitive benchmark study of agentic AI adoption in procurement.

The 2026 Gartner® Magic Quadrant™ for Source-to-Pay Suites named Zycus a Leader. The Forrester Wave™: Supplier Value Management Platforms, Q3 2024 recognised Zycus as a Leader. The IDC MarketScape: Worldwide AI-Enabled Source-to-Pay 2025 Vendor Assessment named Zycus a Leader. And The Hackett Group and Zycus have collaborated on landmark research into agentic AI in procurement, including the 2026 Agentic AI in Procurement Adoption Index built on 250+ global CPO surveys.

These firms do not coordinate. They use different criteria. They reached the same conclusion about this one because the same conclusion was visible to anyone with a serious measurement framework. Four independent lenses, one answer.

The Race Already Run

The race the procurement industry thought it was running — speed versus depth, startups versus suites, AI-native versus enterprise-grade — was the wrong race. The real race was simpler. It was about which platforms recognised that depth was the unfair advantage, and which platforms then did the architectural work to combine that depth with a native agentic layer designed for the era that had just arrived.

That race wasn’t decided by sales demos in 2026. It was decided by architectural choices made — or not made — in the years before most buyers started shopping. By the time the public conversation about agentic procurement reached its current pitch, the platforms that combined enterprise depth with startup speed had already crossed the line.

Explore Zycus’ Procurement Software for Large Enterprises

The CPO sitting through an RFP in 2026 doesn’t have to choose between the two camps anymore. The buyer who insists on choosing between them is solving yesterday’s problem.

The race has already been run. The question now is which platforms the buyer recognises as having finished it.

Related Reads:

- Why Agentic AI Is the Future of Source-to-Pay Automation by 2026

- Agentic AI in Sourcing: What’s Real vs Hype

- Whitepaper: Unlocking Deep Value: The Impact of Agentic AI on Source-to-Pay

- Whitepaper: Beyond GenAI: The Dawn of Agentic AI

- Magazine: Intake to Outcomes (I2O) with Agentic AI-powered Procurement