Budget management in procurement is the process of planning, allocating, tracking, and controlling expenditures against approved spending limits. Procurement budget control ensures that purchasing activities stay within financial boundaries established during the planning cycle. It involves setting budgets by category or cost center, monitoring actual spend against plan, managing variances, and providing visibility to stakeholders on budget consumption throughout the fiscal period.

Read more: Procurement Budget Management Guide: Strategies & Benefits

Why Budget Management Matters in Procurement

Procurement is a primary driver of organizational spending. Without disciplined budget management, purchasing activities can exceed planned expenditures, creating financial surprises and cash flow problems. Effective procurement budget control connects purchasing decisions to financial plans, ensures resources are allocated to priorities, and gives leadership confidence that spending is under control. For procurement teams, budget discipline demonstrates financial stewardship and strengthens credibility with finance partners.

Explore Zycus’ Budget Management Software

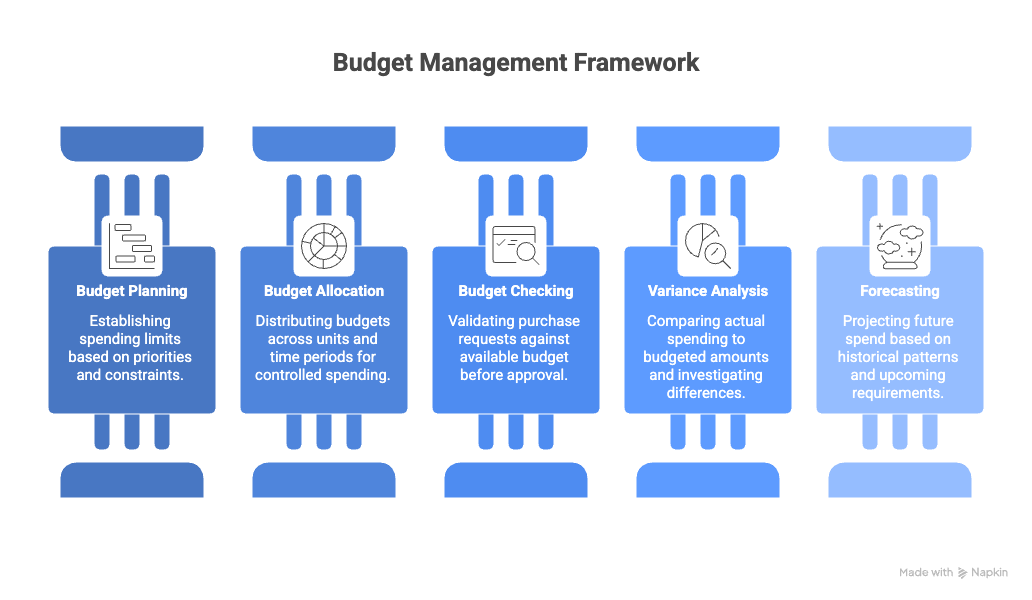

The Core Process of Budget Management

The process begins during annual planning. Procurement works with finance and business units to establish spending budgets by category, department, or project. Historical spend data and forecasts inform budget allocations.

Once budgets are approved, they are loaded into procurement and financial systems. Budget codes are assigned to cost centers, categories, and projects, creating the structure against which actual spending will be tracked.

During execution, each purchase requisition and order is validated against the available budget. Procurement systems check budget availability before approvals proceed, preventing commitments that would exceed limits.

Throughout the period, budget consumption is monitored. Procurement reports on actual versus planned spending, investigates variances, and works with stakeholders to reallocate funds when priorities shift or unexpected needs arise.

Key Benefits of Budget Management

- Prevents overspending by enforcing budget limits at the point of purchase requisition and approval.

- Improves financial predictability by connecting procurement commitments to planned expenditures throughout the fiscal year.

- Enables informed trade-offs by providing visibility into where budget is consumed and where capacity remains for new initiatives.

- Strengthens procurement-finance partnership through shared accountability for spending discipline and accurate forecasting.

- Supports audit and compliance requirements by documenting budget authorizations, approvals, and consumption patterns.

- Reduces budget surprises by tracking committed spend, not just invoiced amounts, for early warning of potential overruns.

Common Pitfalls of Budget Management

Setting unrealistic budgets: Budgets disconnected from actual needs lead to constant exceptions. Base plans on realistic demand forecasts.

Tracking only invoiced spend: Waiting for invoices misses committed spend. Track purchase orders and contracts for early visibility.

Rigid reallocation processes: Business needs change. Enable reasonable budget transfers without excessive bureaucracy.

Disconnected systems: When procurement and finance systems do not integrate, budget visibility is delayed or incomplete.

Elements of Effective Procurement Budget Control

Clear ownership: Every budget line has an accountable owner who approves spending and monitors consumption.

Real-time visibility: Stakeholders can see current budget status without waiting for month-end reports.

Commitment tracking: Open purchase orders and contracts are counted against budget, not just paid invoices.

Threshold alerts: Automatic notifications when spending approaches budget limits, enabling proactive management.

Flexible reallocation: Defined processes for transferring budget between categories when business priorities shift.

KPIs of Budget Management

| Dimension | Sample KPIs |

| Accuracy | Budget variance percentage, forecast accuracy, budget-to-actual ratio |

| Compliance | Percentage of purchases within budget, exception rate, unauthorized spend |

| Visibility | Budget consumption rate, days to close books, reporting timeliness |

| Efficiency | Budget reallocation cycle time, approval turnaround for budget exceptions |

Key Terms in Budget Management

- Budget: A financial plan that allocates resources for spending over a defined period.

- Variance: The difference between budgeted and actual spending, expressed in dollars or percentage.

- Commitment: An obligation to spend created by a purchase order or contract, even before payment occurs.

- Cost Center: An organizational unit or account code to which expenses are charged for tracking purposes.

- Encumbrance: Budget reserved for committed but not yet invoiced spending.

- Reallocation: The transfer of budget from one category or cost center to another.

Technology Enablement

Modern Source-to-Pay platforms integrate with financial systems to enable real-time budget checking at the point of requisition, automated commitment tracking against open purchase orders and contracts, and consolidated reporting on budget consumption across all procurement activities. This integration eliminates manual reconciliation and provides stakeholders with current budget status on demand.

FAQs

Q1. What is budget management in procurement?

The process of planning, allocating, tracking, and controlling procurement spending against approved financial limits throughout the fiscal period.

Q2. Who is responsible for procurement budgets?

Typically shared between procurement, finance, and business unit leaders who own specific budget lines and approve expenditures.

Q3. What is the difference between budget and actual spend?

Budget is the planned allocation. Actual spend is what has been invoiced and paid. Committed spend includes open purchase orders not yet invoiced.

Q4. How often should budgets be reviewed?

Monthly for variance analysis, with formal reforecasting quarterly or when significant business conditions change.

Q5. What happens when a purchase exceeds budget?

Depending on policy, it may be blocked, require exception approval from higher authority, or trigger budget reallocation from other categories.

Q6. How do procurement savings affect budgets?

Savings may reduce budget needs for the category, be reallocated to fund other organizational priorities, or return to corporate reserves.

References

For further insights into these processes, explore the following Zycus resources related to Budget Management: